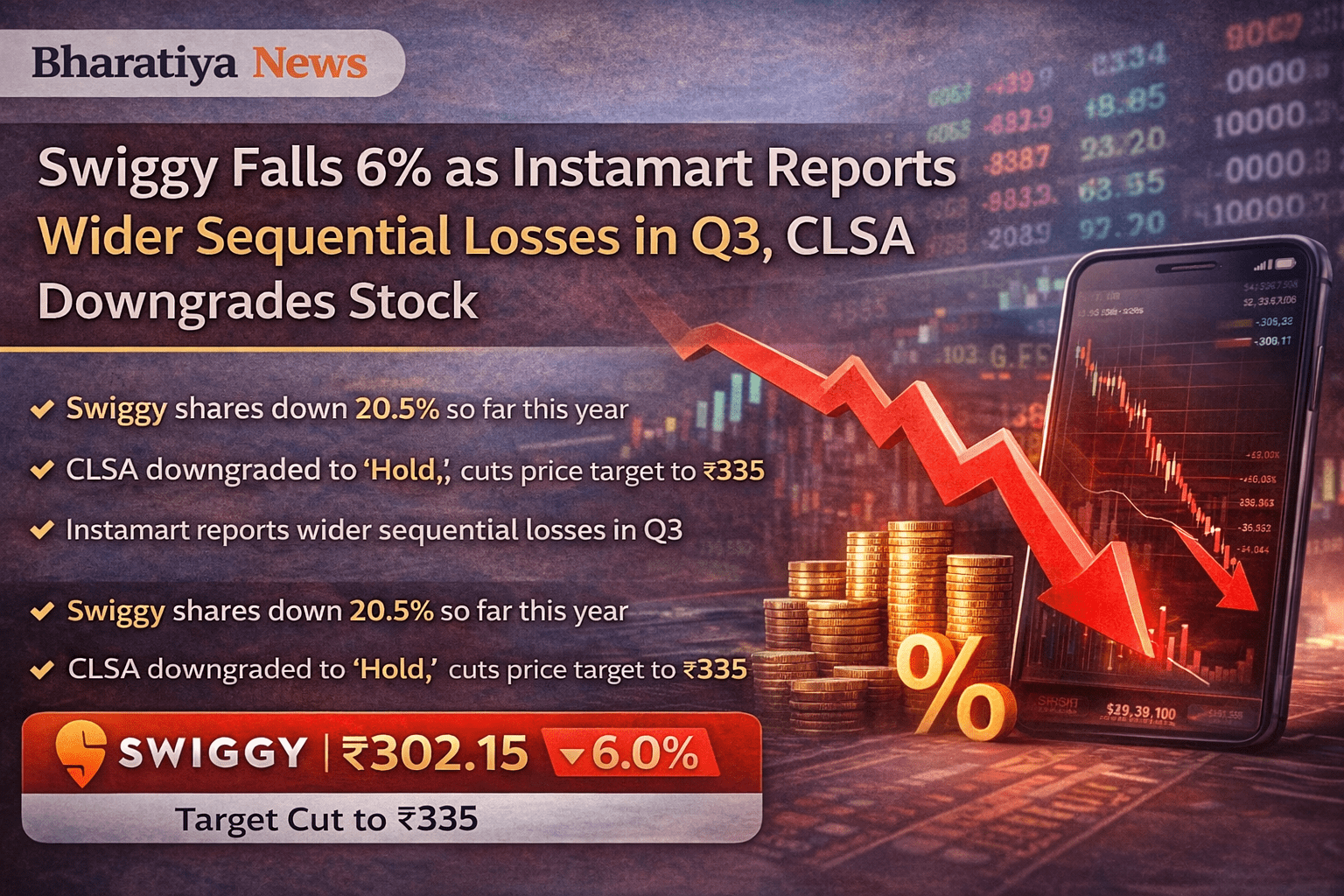

Swiggy Shares Slide 6% After Instamart Losses Widen in Q3; CLSA Downgrades Stock

Shares of food delivery and quick commerce company Swiggy fell sharply on Friday after its quick commerce arm Instamart reported wider sequential losses for the third quarter, prompting global brokerage CLSA to downgrade the stock.

Swiggy’s stock declined nearly 6% during intraday trade, hitting a low of around ₹302 on the NSE, as investors booked profits following three consecutive sessions of gains. The stock has now fallen over 20% so far in 2026, reflecting growing concerns around profitability in the quick commerce segment.

CLSA Downgrades Swiggy to ‘Hold’

CLSA downgraded Swiggy from its earlier rating to ‘Hold’ and reduced its target price to ₹335, citing weaker-than-expected performance in the December quarter. The brokerage noted that Swiggy missed its revenue and EBITDA estimates for Q3, primarily due to underperformance at Instamart.

While Swiggy’s core food delivery business showed steady growth in gross order value and revenues, margins remained largely in line with expectations. However, the quick commerce business disappointed across key metrics, including growth momentum and profitability.

Instamart Losses Remain a Key Concern

Instamart, Swiggy’s largest revenue-generating vertical, reported wider EBITDA losses on a sequential basis, despite some improvement in contribution margins. Analysts pointed out that the path to profitability for quick commerce appears increasingly challenging amid intense competition and high operating costs.

CLSA added that although Swiggy has reiterated its guidance for achieving contribution margin breakeven, the journey toward that goal now looks steeper than earlier anticipated.

Mixed Brokerage Views on Outlook

Other brokerages offered mixed reactions to Swiggy’s quarterly performance. While some highlighted improving margins and narrowing consolidated losses, others raised concerns about the sustainability of profitability in the quick commerce segment.

Swiggy, at a consolidated level, reported a narrower sequential loss and reaffirmed its outlook to achieve contribution margin breakeven by Q1 FY27. However, analysts cautioned that execution risks remain, particularly in Instamart’s expansion strategy.

Stock Performance

With Friday’s decline, Swiggy’s shares continue to remain under pressure in 2026, reflecting investor caution over earnings visibility and the long-term profitability of its quick commerce operations.

(Except for the headline, this story has not been edited by Bharatiya News staff and is published from a syndicated feed.)